Category: Diversification

The Importance of Diversification

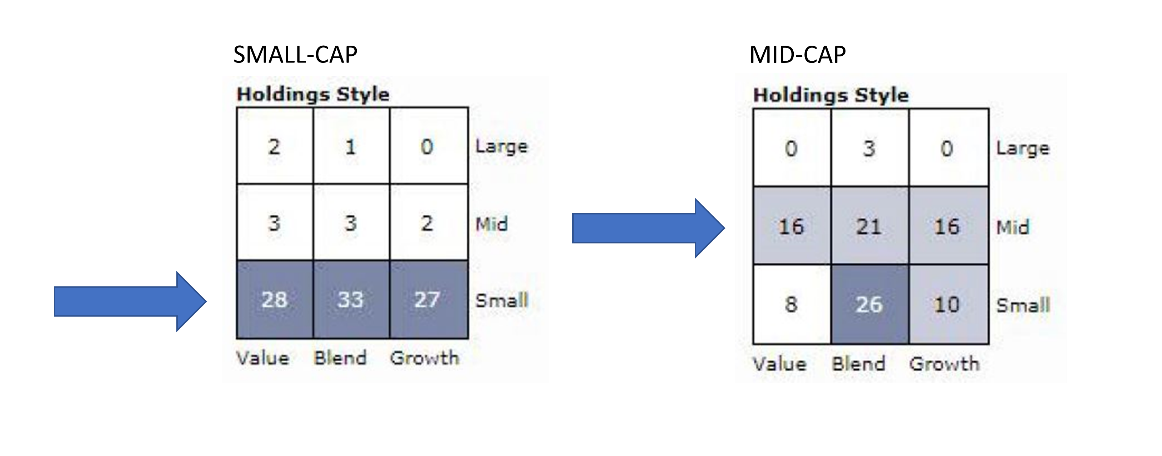

Many people think their investments are diversified, but when you dig deeper on any given portfolio, we find that’s often not the case. In order to diversify your portfolio, you want to choose a variety of assets – stocks, bonds, cash and others – but you also want to choose ones whose returns haven’t all historically moved in the same direction, and, ideally, assets whose returns typically move in opposite directions to hold up your portfolio hold up better in down markets. That way, even if a portion of your portfolio is declining, the rest of your portfolio, hopefully, is growing, and you can potentially offset some of the impact of poor performance on your overall portfolio. Another important aspect of building a well-diversified portfolio is that you try to stay diversified within each type of investment. For example, in terms of your individual stock holdings, beware of overconcentration in a single stock. We usually advise our clients that a single security shouldn’t account for more than 5% of your stock portfolio, unless it’s with the company you work for, and even then, you should limit it to 25%. It’s also smart to diversify across stock holdings by market capitalization (including small, medium, and large caps), sector, and geography. Another important consideration is stock overlap or duplication between funds. This often leads investors to believe they are diversified, when in fact th

![]()

Terms and Conditions | Privacy Policy | Disclosures

Case studies are intended to illustrate the types of financial issues faced by actual clients. They should not be construed as a testimonial for or endorsement of Lineweaver Wealth Advisors. They do not represent the experience of any advisory client. Each client’s situation is different, and their goals may not always be achieved. Lineweaver Wealth Advisors, LLC, is not engaged in the practice of law or accounting. Tax information provided is general in nature and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. Tax rules and regulations are subject to change at any time.

Crain's Cleveland Business is a print and online newspaper delivering local business news and information to Cleveland's business executives, which is published by Crain Communications Inc. The Crain's list may employ different methodology than described above for similar designations granted in other years. No clients were consulted and no fees were paid to determine the winners; the award is based on assets under management. Neither the participating candidates nor their employees pay a fee in exchange for inclusion on Crain's List. However, recipients may pay a fee to Crain, an affiliate, or an unaffiliated third party in exchange for plaques or article reprints commemorating the designation. The publication should not be construed by a client or prospective client as a guarantee that they will experience a certain level of results if the recipient is engaged, or continues to be engaged, to provide investment advisory services; and should not be construed as a current or past endorsement of the recipient by any of its clients. In 2025, 2024, 2020 and 2019 Lineweaver Wealth Advisors (“LWA”) was ranked in the Top 25 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. In 2023, LWA was ranked in the Top 15 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. In 2021 and 2022, LWA was ranked in the Top 20 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. For all years the awards were based on assets under management.

Nominees in the Top 100 Magazine selections are not required to pay a fee for consideration. Individuals appearing in half and full page editorials, have paid a fee for additional exposure. Candidates for consideration are selected utilizing proprietary software. Top 100 Magazine analyzes the results before making their final selections. Financial Professionals and/or wealth managers must also met the following criteria; 1. Be registered with the SEC as a registered investment advisor or a registered investment advisor representative; 2. Have no more than 1 filed complaint with a regulatory agency; 3.Never been convicted of a felony. Third-party rankings and recognitions are no guarantee of future investment success and do not ensure that a client or prospective client will experience a higher level of performance or results. These ratings should not be construed as an endorsement of the Financial Professional by any client nor are they representative of any one client's evaluation. Participants for the Top 100 in Finance appearance were reviewed in 2022, and recognized in March of 2023. Lineweaver Financial Group appeared in Money magazine in 2015, Fortune Magazine in 2016, WTAM 1100 in 2018, Forbes in 2020, Channel 5 in 2020, and Top 100 in Finance in 2023.

Lineweaver Financial Group ©

Powered by  Virteom

Virteom