Many people think their investments are diversified, but when you dig deeper on any given portfolio, we find that’s often not the case.

In order to diversify your portfolio, you want to choose a variety of assets – stocks, bonds, cash and others – but you also want to choose ones whose returns haven’t all historically moved in the same direction, and, ideally, assets whose returns typically move in opposite directions to hold up your portfolio hold up better in down markets. That way, even if a portion of your portfolio is declining, the rest of your portfolio, hopefully, is growing, and you can potentially offset some of the impact of poor performance on your overall portfolio.

Another important aspect of building a well-diversified portfolio is that you try to stay diversified within each type of investment. For example, in terms of your individual stock holdings, beware of overconcentration in a single stock. We usually advise our clients that a single security shouldn’t account for more than 5% of your stock portfolio, unless it’s with the company you work for, and even then, you should limit it to 25%. It’s also smart to diversify across stock holdings by market capitalization (including small, medium, and large caps), sector, and geography.

Another important consideration is stock overlap or duplication between funds. This often leads investors to believe they are diversified, when in fact they may not be. For example, these 3 funds are fairly diversified on their own. But if you were dig a bit deeper on all three of these, you might notice that the first 5-6 of the top 10 stocks within each are the same.

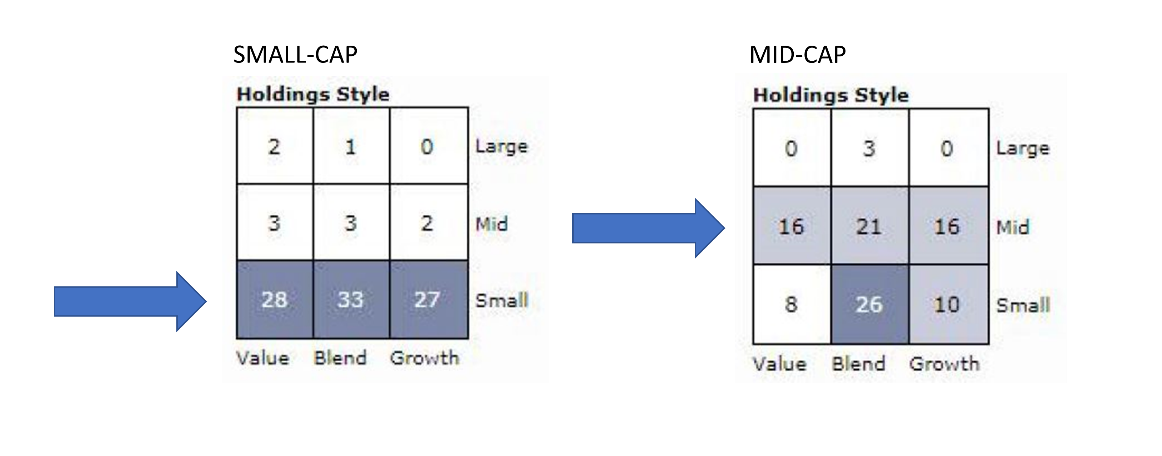

Another issue that most investors aren’t aware of is what we call “style drift.” This happens when a fund gets away from its specified investment style or objective. For example, a small cap company may purchase a mid or small-cap, and then hold onto it. As these stocks grow over time, their market capitalization stock price and number of shares outstanding will grow, and it may become a mid or even large cap. Therefore, losing the small-cap concentration you may have wanted in your portfolio.

Diversification may sound simple, but it can be extremely complicated. We work with many clients who are in or near retirement with portfolios of $500,000 or more. This is always an important consideration at that level. In fact, we have software that specifically analyzes your portfolio from every angle to help you understand if you’re over concentrated in any areas, and help manage your level of risk. This is a particularly complicated part of wealth management, and it takes a Financial Quarterback to drill down and really make sure you’re truly diversified.

Hopefully these tips will help you save some time, money, and stress this holiday season! If you have questions, you can contact us by clicking here, sending an email to quarterback@lineweaver.net, or calling us at (216) 520-1711.