Powell says Fed is “well positioned to wait and see”

By Chad Roope, CFA ®

Chief Investment Officer

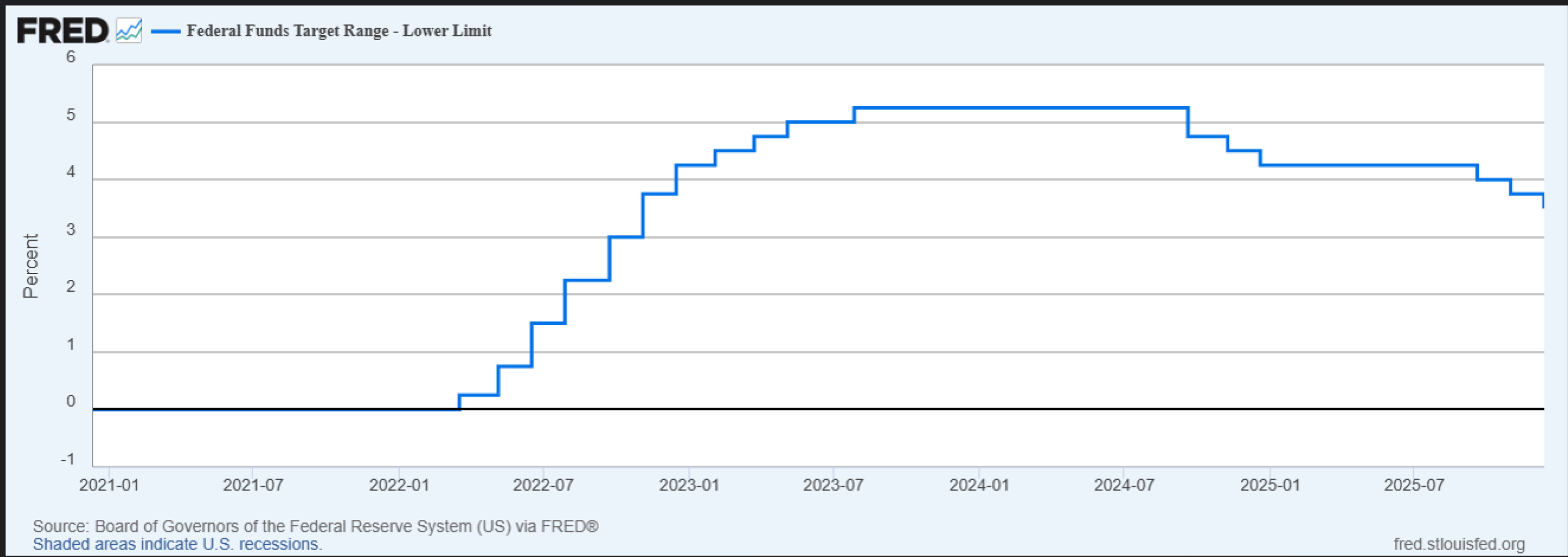

On Wednesday, Dec. 10, the Federal Reserve (Fed) cut the Fed Funds Rate by one-quarter of a point (0.25%) to 3.5% as widely expected. The Fed Funds Rate is the baseline interest rate the Fed sets to control other interest rates and money supply throughout the economy. Lower interest rates usually stimulate economic growth as they make money less expensive to borrow, and higher interest rates usually slow economic growth as they make money more expensive to borrow. The Fed raises and lowers rates to try and balance inflation and employment, with the goal of fostering solid economic growth that supports full employment without stoking excessive inflation. As seen in the chart below, the Fed has now cut rates by 1.75% from 5.25% to 3.5% since September 2024, after an aggressive hiking cycle and pause that started in March 2022.

The hikes that started in March 2022 were designed to slow economic growth to stave off one of the largest inflation spikes in U.S. history post-COVID. The Fed then judged in September 2024 that the mission had largely been accomplished and that rates needed to come down to support employment and the economy.

Now, however, we have likely entered a new phase. Fed Chairman Jerome Powell indicated last Wednesday that the Fed is now “well positioned to wait and see” given the rate reductions since September 2024. We think this means they will hold interest rates steady for some time until economic data changes sufficiently in either direction to warrant a change. It appears the Fed now thinks employment, inflation and the economy are roughly in balance. In fact, they slightly increased their projections of economic growth in 2026 and noted that a recent uptick in inflation is mostly related to one-time effects of tariffs. Only the future will tell if their judgment proves accurate, but we generally agree with their assessment at present.

We will post our 2026 Outlook in January, but broadly, we expect the economy and earnings to remain solid in 2026, which should support financial markets. The Fed cuts over the last year or so are just now beginning to work in the economy, which should be supportive. We also expect tax cuts from 2025 Washington tax legislation to be stimulative in early 2026 as well. As such, our base case calls for solid, but more modest financial market performance in 2026, with diversifying asset classes potentially playing a larger role. More to come in January.

Sources:

https://fred.stlouisfed.org/series/DFEDTARL#

https://www.federalreserve.gov/newsevents/pressreleases/monetary20251210a.htm

![]()

Terms and Conditions | Privacy Policy | Disclosures

Case studies are intended to illustrate the types of financial issues faced by actual clients. They should not be construed as a testimonial for or endorsement of Lineweaver Wealth Advisors. They do not represent the experience of any advisory client. Each client’s situation is different, and their goals may not always be achieved. Lineweaver Wealth Advisors, LLC, is not engaged in the practice of law or accounting. Tax information provided is general in nature and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. Tax rules and regulations are subject to change at any time.

Crain's Cleveland Business is a print and online newspaper delivering local business news and information to Cleveland's business executives, which is published by Crain Communications Inc. The Crain's list may employ different methodology than described above for similar designations granted in other years. No clients were consulted and no fees were paid to determine the winners; the award is based on assets under management. Neither the participating candidates nor their employees pay a fee in exchange for inclusion on Crain's List. However, recipients may pay a fee to Crain, an affiliate, or an unaffiliated third party in exchange for plaques or article reprints commemorating the designation. The publication should not be construed by a client or prospective client as a guarantee that they will experience a certain level of results if the recipient is engaged, or continues to be engaged, to provide investment advisory services; and should not be construed as a current or past endorsement of the recipient by any of its clients. In 2025, 2024, 2020 and 2019 Lineweaver Wealth Advisors (“LWA”) was ranked in the Top 25 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. In 2023, LWA was ranked in the Top 15 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. In 2021 and 2022, LWA was ranked in the Top 20 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. For all years the awards were based on assets under management.

Nominees in the Top 100 Magazine selections are not required to pay a fee for consideration. Individuals appearing in half and full page editorials, have paid a fee for additional exposure. Candidates for consideration are selected utilizing proprietary software. Top 100 Magazine analyzes the results before making their final selections. Financial Professionals and/or wealth managers must also met the following criteria; 1. Be registered with the SEC as a registered investment advisor or a registered investment advisor representative; 2. Have no more than 1 filed complaint with a regulatory agency; 3.Never been convicted of a felony. Third-party rankings and recognitions are no guarantee of future investment success and do not ensure that a client or prospective client will experience a higher level of performance or results. These ratings should not be construed as an endorsement of the Financial Professional by any client nor are they representative of any one client's evaluation. Participants for the Top 100 in Finance appearance were reviewed in 2022, and recognized in March of 2023. Lineweaver Financial Group appeared in Money magazine in 2015, Fortune Magazine in 2016, WTAM 1100 in 2018, Forbes in 2020, Channel 5 in 2020, and Top 100 in Finance in 2023.

Lineweaver Financial Group ©

Powered by  Virteom

Virteom