November Market Commentary

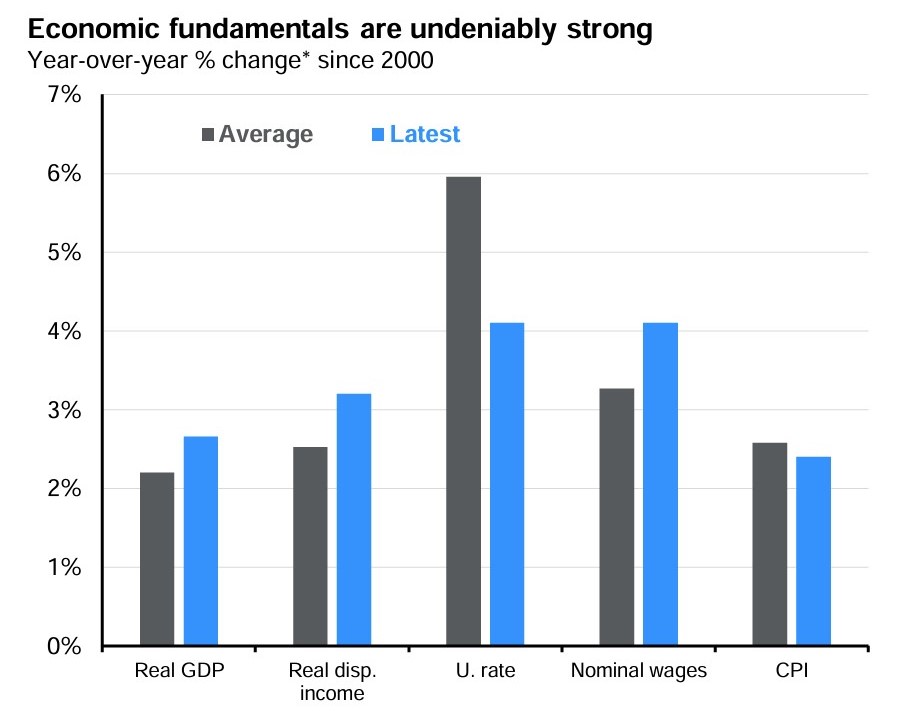

As the dust settles post-election, investors are keenly assessing what the next four years might bring. Despite the policy uncertainties that accompany a unified Republican government, the economic outlook remains largely stable. Additionally, market fundamentals look strong and matter more for returns, especially over the long term. The U.S. economy continues to be a straight A student, with GDP growth above trend (3Q24: 2.8% q/q saar), full employment (October unemployment rate: 4.1%), and low inflation (September CPI: 2.4% y/y), as shown in the chart below.

Consumers are maintaining their spending habits despite dissatisfaction with mortgage rates, which are higher than before the pandemic, and the price increases of the past few years. However, this confidence may be shifting, as evidenced by the Consumer Confidence Index's significant monthly increase—the largest since March 2021—rising to 108.7 in October from 99.2 in September. Notably, all five components of the index improved, indicating growing confidence in future job availability and stock market gains.

This economic environment is favorable for equity markets. Declining interest rates and real wage gains are positive for consumer spending, and S&P 500 operating margins are 8% above long-term averages, showcasing the dynamism of U.S. companies. Additionally, secular trends continue to encourage corporate investment. Besides high valuations, there are few reasons to anticipate a disruption in the upward trajectory of equities. The effects of the new administration's policies won’t be apparent for a while, so investors should refocus on the fundamentals, which are undeniably strong.

Source: JP Morgan Asset Management, which used sources BEA, BLS, J.P. Morgan Asset Management, Conference Board, S&P. All figures are y/y change, except for the unemployment rate (U.rate), which is a ratio. Nominal wages: Avg. hourly earnings of production and non-supervisory workers.

![]()

Terms and Conditions | Privacy Policy | Disclosures

Case studies are intended to illustrate the types of financial issues faced by actual clients. They should not be construed as a testimonial for or endorsement of Lineweaver Wealth Advisors. They do not represent the experience of any advisory client. Each client’s situation is different, and their goals may not always be achieved. Lineweaver Wealth Advisors, LLC, is not engaged in the practice of law or accounting. Tax information provided is general in nature and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. Tax rules and regulations are subject to change at any time.

Crain's Cleveland Business is a print and online newspaper delivering local business news and information to Cleveland's business executives, which is published by Crain Communications Inc. The Crain's list may employ different methodology than described above for similar designations granted in other years. No clients were consulted and no fees were paid to determine the winners; the award is based on assets under management. Neither the participating candidates nor their employees pay a fee in exchange for inclusion on Crain's List. However, recipients may pay a fee to Crain, an affiliate, or an unaffiliated third party in exchange for plaques or article reprints commemorating the designation. The publication should not be construed by a client or prospective client as a guarantee that they will experience a certain level of results if the recipient is engaged, or continues to be engaged, to provide investment advisory services; and should not be construed as a current or past endorsement of the recipient by any of its clients. In 2025, 2024, 2020 and 2019 Lineweaver Wealth Advisors (“LWA”) was ranked in the Top 25 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. In 2023, LWA was ranked in the Top 15 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. In 2021 and 2022, LWA was ranked in the Top 20 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. For all years the awards were based on assets under management.

Nominees in the Top 100 Magazine selections are not required to pay a fee for consideration. Individuals appearing in half and full page editorials, have paid a fee for additional exposure. Candidates for consideration are selected utilizing proprietary software. Top 100 Magazine analyzes the results before making their final selections. Financial Professionals and/or wealth managers must also met the following criteria; 1. Be registered with the SEC as a registered investment advisor or a registered investment advisor representative; 2. Have no more than 1 filed complaint with a regulatory agency; 3.Never been convicted of a felony. Third-party rankings and recognitions are no guarantee of future investment success and do not ensure that a client or prospective client will experience a higher level of performance or results. These ratings should not be construed as an endorsement of the Financial Professional by any client nor are they representative of any one client's evaluation. Participants for the Top 100 in Finance appearance were reviewed in 2022, and recognized in March of 2023. Lineweaver Financial Group appeared in Money magazine in 2015, Fortune Magazine in 2016, WTAM 1100 in 2018, Forbes in 2020, Channel 5 in 2020, and Top 100 in Finance in 2023.

Lineweaver Financial Group ©

Powered by  Virteom

Virteom